Qualified charitable distributions (QCDs) from an IRA offer individual over 70½ with a valuable method to achieve income tax savings on charitable donations, even if they choose to utilize the newly increased standard deduction. The significance of QCDs has grown in the context of recent tax law changes, providing a unique opportunity for older taxpayers to contribute to charitable causes while reaping tax benefits.

The Landscape of Charitable Giving Post-TCJA

The number of individuals claiming charitable deductions on their taxes has seen a notable decline, falling below 70% for the fourth consecutive year according to “Giving USA 2022: The Annual Report on Philanthropy.” This downward trend is largely attributed to the Tax Cut and Jobs Act (TCJA) of 2017. Before the TCJA, the Tax Policy Center estimated that around 37 million households itemized their deductions in 2017. However, post-TCJA, this number dropped dramatically to about 16 million in 2018.

The TCJA introduced several significant changes, but the two most critical in terms of charitable giving are: (1) the limitation of the itemized tax deduction for state and local taxes (SALT) to $10,000 per return, and (2) the substantial increase in the standard deduction, which rose from $6,350 in 2017 to $13,850 in 2023 for individuals, and from $12,700 to $27,700 for married couples filing joint returns. This shift has made it more advantageous for most taxpayers to take the standard deduction rather than itemizing their deductions. Consequently, an estimated 90% of taxpayers are expected to opt for the standard deduction in future years.

Impact on Charitable Contributions

The increased use of the standard deduction has effectively disincentivized charitable contributions, as taxpayers often do not receive deductions for their donations. According to the conservative think tank AEI, “Many taxpayers who otherwise would have deducted their charitable donations as itemizers will now claim the standard deduction and not receive a tax incentive for charitable giving.”

The Silver Lining: Qualified Charitable Distributions

Fortunately, for those over 70½ who wish to donate to charity and still gain tax relief, the law remains unchanged regarding charitable gifts from retirement accounts, specifically IRAs. Individuals in this age group can make charitable donations directly from their IRAs to their chosen charities without recognizing the distribution as taxable income. This provision allows these individuals to enjoy a tax benefit from their donations, even if they opt for the standard deduction.

The IRS defines a QCD as “an otherwise taxable distribution from an IRA…owned by an individual who is age 70½ or over that is paid directly from the IRA to a qualified charity.” Through QCDs, individuals can donate up to $100,000 annually from their retirement accounts, a limit that exceeds the typical donation amount for most taxpayers.

The Growing Relevance of QCDs

While QCDs have been available for some time, their significance has surged with the passage of the TCJA and the resulting increase in the standard deduction. Going forward, it will be more beneficial for individuals who take the standard deduction to use their IRAs for charitable contributions. For example, an individual can make a charitable gift from their IRA, applying the donation towards satisfying their required minimum distribution for the year without incurring income tax on the distribution, as the funds go directly to the charity.

This tax-efficient strategy works because the law allows individuals over 70½ to make direct charitable gifts from their IRAs to eligible charities, excluding these distributions from their gross income. Although required minimum distributions (RMDs) do not begin until age 73 or 75, depending on the year of birth, QCDs offer a powerful way to support charities while reducing taxable income.

Additional Benefits of QCDs

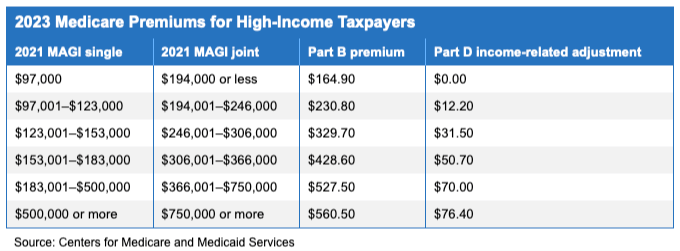

Beyond income tax savings, QCDs can also potentially reduce Medicare premiums. High-income earners often face increased Medicare premiums when their income exceeds certain thresholds. A QCD can help lower their modified adjusted gross income (MAGI), which in turn can reduce Medicare premiums in future years.

For instance, consider a couple earning a combined $245,000 per year. If their last IRA withdrawal pushes their MAGI above the $247,000 threshold, their Medicare premiums could spike by over $2,500 for one year. However, if they make a $5,000 charitable donation through a QCD, reducing their MAGI to $240,000, their Medicare premiums could be lowered, potentially saving them $2,500 annually. It's important to note that Medicare premiums are based on tax returns from two years prior.

Technical Requirements for QCDs

To ensure a QCD qualifies for special tax treatment, several technical requirements must be met:

- Direct Payment to Charity: The QCD check must be made payable directly to the charity from the IRA account. It cannot be distributed to the taxpayer first and then donated. However, if the IRA owner has check-writing privileges on their traditional IRA, they might be able to write the check directly to the charity themselves.

- Eligible Charities: The charity must be a 501(c)(3) organization. Private foundations and donor-advised funds do not qualify for QCDs.

- IRA Custodian Requirements: It's essential to check with the IRA custodian for any additional specific requirements or forms necessary to execute a successful QCD.

Strategic Use of QCDs

Overall, while QCDs have been somewhat niche in the past, the TCJA has significantly increased their relevance, making them a more useful tool for taxpayers moving forward. Individuals taking the standard deduction and over the age of 70½ who still want a tax break for charitable donations can use QCDs to give directly from their IRAs to their chosen charities, achieving tax savings and fulfilling charitable goals simultaneously. Additionally, by strategically timing their donations, they may also benefit from reduced Medicare premiums.

Maximizing the Benefits of QCDs

To maximize the benefits of QCDs, individuals should consider their overall tax and financial situation. For example, those nearing the age of 73 or 75 (depending on their birth year) should plan their QCDs in conjunction with their RMDs. By doing so, they can effectively reduce their taxable income while satisfying their RMD requirements.

Furthermore, individuals should consult with their financial advisors or tax professionals to ensure they are making the most of their QCDs. Advisors can provide guidance on the optimal amount to donate, the timing of donations, and how to integrate QCDs into their broader financial strategy.

Case Studies

To illustrate the impact of QCDs, consider the following hypothetical scenarios:

Case Study 1: Reducing Taxable Income

- Jane is 72 years old and has an IRA with a balance of $500,000. She is required to take an RMD of $20,000 this year. Jane decides to donate $15,000 to her favorite charity via a QCD. As a result, she only needs to withdraw an additional $5,000 to meet her RMD requirement. The $15,000 QCD is excluded from her taxable income, significantly reducing her tax liability.

Case Study 2: Lowering Medicare Premiums

- John and Mary, both in their mid-70s, have a combined annual income of $250,000. They are aware that crossing the $247,000 MAGI threshold will increase their Medicare premiums. To avoid this, they make a $10,000 charitable donation through a QCD, reducing their MAGI to $240,000. This strategic move helps them avoid the Medicare premium increase, saving them money in the long run.

Future Considerations

As tax laws and regulations evolve, it's essential to stay informed about changes that may impact QCDs and charitable giving strategies. Legislative changes could alter the landscape of tax incentives for charitable donations, making it even more crucial to work with financial professionals who can navigate these complexities.

In conclusion, QCDs offer a powerful tool for individuals over 70½ to support charitable causes while achieving significant tax savings. In the wake of the TCJA and the increased standard deduction, QCDs have become an even more valuable strategy for maximizing the benefits of charitable giving. By understanding the requirements and potential benefits of QCDs, individuals can make informed decisions that align with their financial goals and philanthropic aspirations.